Télécharger la présentation

La présentation est en train de télécharger. S'il vous plaît, attendez

1

Government policy

2

Breaking News Mario Draghi (3 September 1947), President of the European Central Bank since 1 November 2011 PHD in the MIT Vice chairman and managing director of Goldman Sachs International and a member of the firm-wide management committee (2002– 2005)

, President of the European Central Bank since 1 November 2011 PHD in the MIT Vice chairman and managing director of Goldman Sachs International and a member of the firm-wide management committee (2002– 2005)")

3

Loukas Papadimos (1947) Prime minister of Greece since november 2011 PHD in the MIT 1994 – 2002 : governor of the Bank of Greece (when Greece cheated to enter the Eurozone)

Prime minister of Greece since november 2011 PHD in the MIT 1994 – 2002 : governor of the Bank of Greece (when Greece cheated to enter the Eurozone)")

4

Mario Monti (1943) : new Italian Premier Studied in Yale (under Jame Tobin) European commissioner International adviser to Goldman Sachs since 2005

: new Italian Premier Studied in Yale (under Jame Tobin) European commissioner International adviser to Goldman Sachs since 2005")

5

What can the government do ? Monetary policy : money supply and interest rate (this is in the hands of Mr Mario Draghi) Fiscal policy : Taxes and spending (very difficult in a high debt configuration) Nationalisation Regulation Like in football, you can be a player, the referee or the author of the rules.

Fiscal policy : Taxes and spending (very difficult in a high debt configuration) Nationalisation Regulation Like in football, you can be a player, the referee or the author of the rules..")

6

Government Purchases (G), Net Taxes (T), and Disposable Income (Y d ) AE = C+I+G

, Net Taxes (T), and Disposable Income (Y d ) AE = C+I+G")

7

Budget deficit ≡ G − T Saving/investment approach to equilibrium : S + T = I + G

8

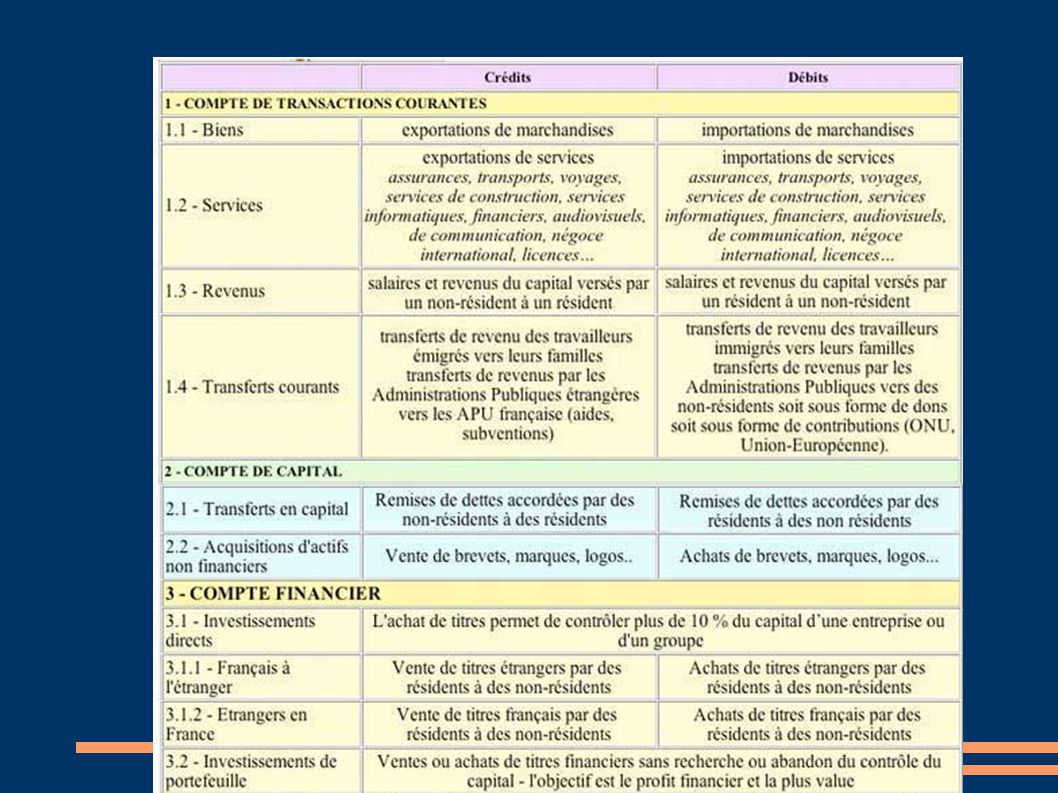

Balance of payments The record of all financial moves due to export, import, investment, travels... Two main accounts Current account Capital account

9

Current account Balance exports - imports + net income from assets - net transfers to foreigners (remittance)

")

10

Méthodologie de la balance des paiements, Banque de France (novembre 2005) Par convention, un chiffre positif (crédit) correspond à une exportation ou à une recette lorsqu’il se rapporte à une opération réelle, c’est-à-dire à des échanges de biens, de services et des paiements de revenus. Un chiffre négatif (débit) représente une importation ou une dépense. S’agissant du compte financier, un chiffre positif reflète une diminution des avoirs ou une augmentation des engagements, qu’ils soient financiers ou monétaires. Un chiffre négatif représente une augmentation des avoirs ou une diminution des engagements. Ainsi, un chiffre négatif au titre des avoirs de réserve signifie-t-il que les réserves ont augmenté.

représente une importation ou une dépense. S’agissant du compte financier, un chiffre positif reflète une diminution des avoirs ou une augmentation des engagements, qu’ils soient financiers ou monétaires. Un chiffre négatif représente une augmentation des avoirs ou une diminution des engagements. Ainsi, un chiffre négatif au titre des avoirs de réserve signifie-t-il que les réserves ont augmenté..")

12

Capital account Balance records the flow of capital borrowing, lending, selling, purchasing Foreign funds entering a country from the sale or purchase of tangible assets - as opposed to non-physical assets such as stocks or bonds - are recorded in the capital account of the BOP. The account is positive when we sell the country's assets to foreigners.

13

Capital account deficit = More investment abroad than saving at home Investing for the future or living on other people's expenses ? But dividends are also debits in the current account (and sign of a healthy economy).

..")

14

Source : http://www.banque-france.fr

15

Charles Gave (http://www.geostrategique.net) Ce qui veut dire en termes simples que la balance commerciale d’un pays ou les sociétés s’organisent selon les principes de la plate forme, ne veut plus rien dire, ce qui ne manque pas de piquant quand l’on voit la baisse actuelle du dollar engendrée, parait-il, par les déficits de la balance commerciale… Les marchés n’ont pas compris que nous sommes en train d’assister à la privatisation des balances commerciales. Ce qui veut dire en termes simples que quiconque reste enfermé dans la logique de la comptabilité nationale pour effectuer ses investissements va tout droit à la ruine.

16

It is important to understand the reasons behind the deficit Bad productivity ? Military expenses ? Many different types of deficit. Economists say : Do not mix current account deficit and public deficit. I do.

17

The meaning of the sovereign debt Today, sovereign debt in France for instance is used to subsidize low productivity sectors. But remember the circular flow. Money comes from competitive sectors... goes to households... and finally goes to China ! That's why it is difficult to separate the different debts.

18

Distortions ? The government can affect investment behavior through its tax treatment of depreciation and other tax policies. Market is the defining institution of capitalism : it should bring the economy to an equilibrium. Markets allocate ressources and opportunities among competitors. But they need rules.

19

Market failure ? Markets should reflect costs and benefits but - sometimes – they fail to do so. Externalities Incomplete information

20

Y = C + I + G TABLE 24.1 Finding Equilibrium for I = 100, G = 100, and T = 100 300100200250 50 100 450 150 Output ↑ 500100400 0100 600 100 Output ↑ 70010060055050100 750 50 Output ↑ 900100800700100 9000Equilibrium 1,1001001,000850150100 1,050+ 50Output ↓ 1,3001001,2001,000200100 1,200+ 100Output ↓ 1,5001001,4001,150250100 1,350+ 150Output ↓ Government in the Economy The Determination of Equilibrium Output (Income)

")

21

Multiplier for policy-makers The Government Spending Multiplier The tax Multiplier The Balanced-Budget Multiplier But taxes depend on income : the effect of the multiplier is lower than in a simple model

23

Il me semble qu’on en revient ici encore aux limites des raisonnements macroéconomiques trop généraux : ils ne prennent pas en compte l’hétérogénéité des investissements publics envisageables. De la même manière, raisonner en terme de « baisse d’impôts » de manière globale n’a pas trop de sens : certaines baisses ciblées auront plus d’impact que d’autres. Enfin, un tout dernier point mérite d’être souligné. Rien ne dit que la valeur des différents multiplicateurs soit la même en période de récession qu’en période de croissance « normale ». Il serait bon de voir s’il n’y a pas des travaux cherchant à mesurer et comparer cette valeur suivant le contexte économique.

24

TABLE 24.2 Finding Equilibrium after a Government Spending Increase of 50 (G Has Increased from 100 in Table 9.1 to 150 Here) (1)(2)(3)(4)(5)(6)(7)(8)(9)(10) Output (Income) Y Net Taxes T Disposable Income Y d ≡Y T Consumption Spending C = 100 +.75 Y d Saving S Y d – C Planned Investment Spending I Government Purchases G Planned Aggregate Expenditure C + I + G Unplanned Inventory Change Y (C + I + G) Adjustment to Disequilibrium 300100200250 50 100150500 200 Output ↑ 500100400 0100150650 150 Output ↑ 70010060055050100150800 100 Output ↑ 900100800700100 150950 50 Output ↑ 1,1001001,0008501501001501,1000Equilibrium 1,3001001,2001,0002001001501,250+ 50Output ↓ Fiscal Policy at Work: Multiplier Effects The Government Spending Multiplier

(1)(2)(3)(4)(5)(6)(7)(8)(9)(10) Output (Income) Y Net Taxes T Disposable Income Y d ≡Y T Consumption Spending C = Y d Saving S Y d – C Planned Investment Spending I Government Purchases G Planned Aggregate Expenditure C + I + G Unplanned Inventory Change Y (C + I + G) Adjustment to Disequilibrium 200 Output ↑ 150 Output ↑ 100 Output ↑ 50 Output ↑ 1, , ,1000Equilibrium 1, ,2001, , Output ↓ Fiscal Policy at Work: Multiplier Effects The Government Spending Multiplier")

25

Fiscal policy and bad externalities Common Agricultural Policy 48% of EU's budget. Covers Brittany with pigs factories Covers Alsace with corn fields Covers Brittany's beach with green algae Empties the water tables Destroys African agriculture

26

A complex equilibrium automatic stabilizers Revenue and expenditure items in the federal budget that automatically change with the state of the economy in such a way as to stabilize GDP. automatic destabilizer Revenue and expenditure items in the federal budget that automatically change with the state of the economy in such a way as to destabilize GDP fiscal drag The negative effect on the economy that occurs when average tax rates increase because taxpayers have moved into higher income brackets during an expansion.

27

Deficit targeting changes the way the economy responds to negative demand shocks because it does not allow the deficit to increase. The result is a smaller deficit but a larger decline in income than would have otherwise occurred. Deficit Targeting as an Automatic Destabilizer

28

Monetary policy No inflation Steady growth (no business cycle) Productivity and real GDP per worker growth Capacity utilisation, employment Today most of the central banks target inflation and not money growth. http://www.econlib.org/library/Enc/MonetaryPolicy.html

29

Everything gets more complicated After the 1980-1981 recession, the Europeans acted like monetarist (afraid of inflation) and the Americans like keynesians (pumping money into the system to boost it). There really seems to be a trade-off between inflation and unemployment.

30

The costs of inflation Shoe leather cost (for going to the bank) Tax distorsion (bracket creep*) : real taxes rise faster than the purchasing power. Money illusion (leads to bad decision) Inflation variability : negative effect on bonds (with fixed nominal payment) * progression a froid, effet multiplicateur de l'inflation

Inflation variability : negative effect on bonds (with fixed nominal payment) * progression a froid, effet multiplicateur de l inflation.")

31

The benefits of inflation Seignorage : the tax on money Makes adjustements easier through money illusion (for instance : lowering real wages) Makes negative real interest rate possible

Makes negative real interest rate possible")

32

Monetarist-Keynesian controversy (again) For monetarists, injection of new spending just brings inflation. For Keynesians, raising the demand will bring back to work the involuntarily unemployed.

33

An expansionary policy that should have begun to take effect at point A does not actually begin to have an impact until point D, when the economy is already on an upswing. Hence, the policy pushes the economy to points E and F (instead of points E and F). Income varies more widely than it would have if no policy had been implemented. Time Lags Regarding Monetary and Fiscal Policy

. Income varies more widely than it would have if no policy had been implemented. Time Lags Regarding Monetary and Fiscal Policy.")

34

Recognition lag : the time policy maker need to understand what is going on. Implementation lag : the time need to make the decision and to start action. Response lag : the time it need to be really effective.

35

1 st of january 1999 : the ECB takes over the monetary policy One goal : keep the inflation under 2% One mean : the interest rate But deregulation makes this mission difficult

36

The Taylor rule John Taylor (1946) A rule for monetary policy that links inflation, output and the interest rate. Central banks target inflation rate and no more nominal money growth.

37

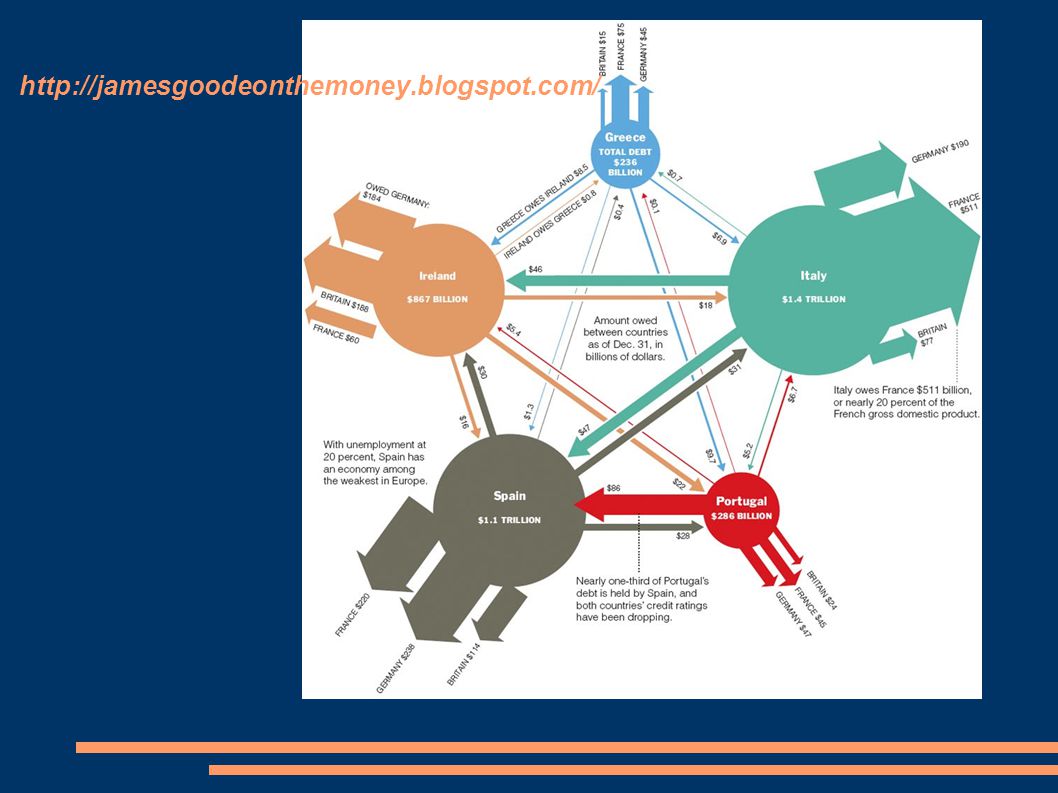

http://jamesgoodeonthemoney.blogspot.com/

38

Is speculation bad for the economy ? http://stopgamblingonhunger.com/

Présentations similaires

- Jean Rauscher>")

that don’t follow the normal rules. Because of this, we have to learn them by heart. Thankfully,>")